With a tax-efficient Individual Savings Account (ISA), anyone can effectively boost their chances of generating a substantial second income in retirement.

Here's one way a person can try and build a £3,000 passive income with tax-free Individual Savings Account (ISA) investments.

Please be aware that tax implications will depend on the specific circumstances of each individual or business. The guidance in this article is provided for general information purposes only and does not constitute professional tax advice. It is the responsibility of readers to conduct their own research and to consult with a qualified professional before making any investment or financial decisions.

Think carefully

To begin with, there's no standard formula for investing or saving. We all have our own distinct short- and long-term investment objectives, alongside differing attitudes towards risk and personal financial situations.

For that reason, some clear rules pertaining to investing are worth heeding.

Saving mainly in Cash ISAs is unlikely to earn a comfortable retirement income for most of us. In simple terms, while our money may be secure in such an account, the returns we can expect are likely to be insufficient, given most people's financial situations.

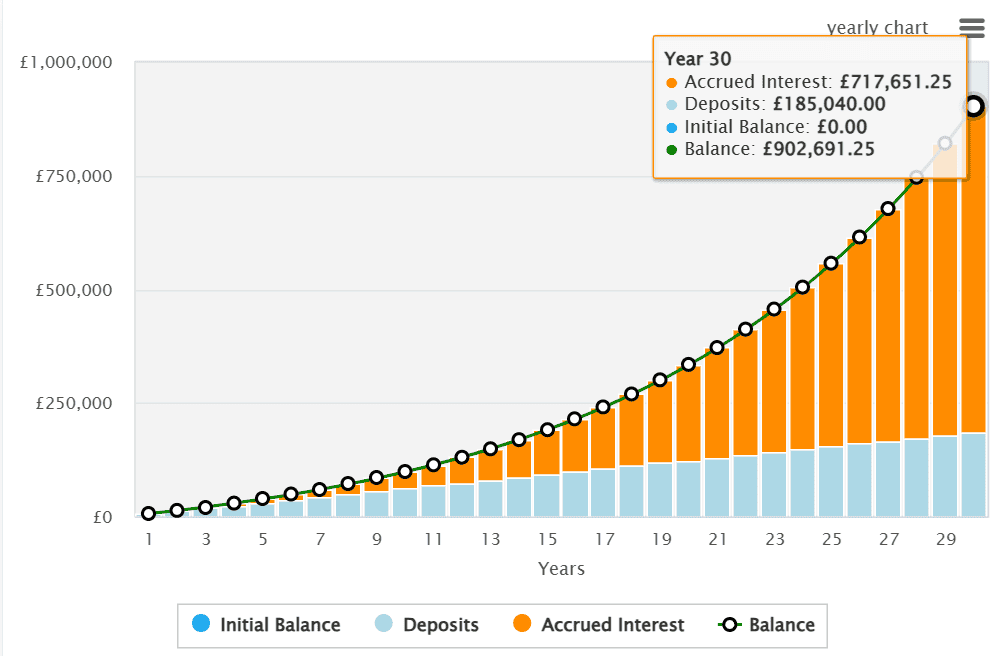

Targeting an annual income of £36,000

Let's say an investor has £514 available each month. This is the average sum that Britons currently save or invest, according to the financial services provider Shepherd's Friendly.

They would, after 30 years, be sitting on £356,741 in their account. Based on a 4% annual withdrawal rate, that would leave them with an income of £14,270, which amounts to £1,189 a month.

As mentioned, such income is assured and secure. Nevertheless, even with the State Pension included, this individual is unlikely to have the £43,100 that the Pensions and Lifetime Savings Association (PLSA) states individuals require to live comfortably in retirement.

or thereabouts by the time they retire.

Based on the same 4% drawdown rate, this £900k balance would provide an average monthly income of £36,000. With the state pension included, the PLSA target of £43,100 could be quite achievable.

.

Investing in funds

That 8.8% return is achievable, in my opinion, based on the proven long-term track record of UK and US shares.

have achieved average returns of 7% and 11% each year. If this trend continues – and, unlike a Cash ISA, this is not a guaranteed outcome – the £514 invested equally between a tracker fund for each index would generate around £3,000 a month in extra income.

This is one such fund that investors can consider today.

At an ongoing charge of 0.07%, it is the cheapest S&P-based ETF currently available in the UK. When combined with a Stocks and Shares ISA, it could save investors a substantial amount of money by eliminating unnecessary fees and taxes.

Investing in any fund is, of course, more precarious than keeping cash. However, by putting your money into 500 different business ventures, you can diversify your investments and potentially earn superior returns while spreading risk.

In this scenario, people lower their chances of experiencing a decline in investment value by diversifying their portfolio across a wide range of companies operating in various sectors and locations. It's worth noting that even with this diversified approach, an investment fund may still decrease in value when the economy is experiencing difficulties. However, owning such a fund can reduce the risk of sudden and extreme fluctuations, potentially leading to a consistently stable return over a more extended period.

It's why I hold a UK equivalent, such as a FTSE 100 fund, in my own Individual Savings Account.

.

More reading

- Will there be a stock market crash and what action should I take now?

us better investors.